healthcare reform

As a trusted benefits administrator, Flexible Benefit Service LLC (Flex) wants to keep you informed on the following:

Federal regulators have recently indicated that they don’t feel the current COBRA notices provide enough information about the Exchanges and the options that COBRA beneficiaries have in the Individual Marketplace.

The Department of Health and Human Services (HHS) issued some new guidance on May 2, 2014 as it relates to Special Enrollment Periods and Hardship Exemptions in the individual marketplace. The new guidance has been summarized below:

On April 1, 2014, President Obama signed into law the “Protecting Access to Medicare Act of 2014.” Although much of the law is designed to fix problems with the Medicare program, the law also included a repeal of the deductible limits that apply to small group health plans. In 2014, the Affordable Care Act (ACA) established deductible limits for health plans offered to small employers (defined as up to 50 employees in most states).

Applies to those who have started the enrollment process and experienced an error

Last week, the Obama administration released several new Affordable Care Act (ACA) guidelines. Of particular note, any individual or small group with a non-ACA compliant plan will be able to keep that plan in place for additional time.

Can people apply for individual health coverage after Mar. 31, 2014?

Only those individuals that experience a qualifying event can sign up for a qualified health plan mid-year after March 31st. Most qualifying events will create a special enrollment period that lasts for 60 days.

Today is the last day of February which means we are only one month away from the end of the first open enrollment period for individual health plans. March 31st is the last day that individuals can sign up for coverage without a qualifying event, but there is one big question that is still looming – Will the open enrollment period get extended to a later date?

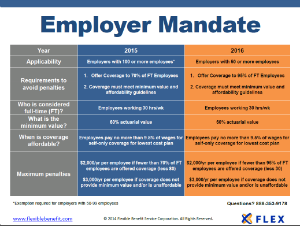

Yesterday, IRS officials made a significant announcement that impacts the Employer Shared Responsibility requirements, also known as the Employer Mandate. New guidance issued by the IRS confirms that a new phased approach will be utilized to implement it.

The new approach has 3 significant changes to the previously written rules: